So much for “April Showers.” April was about resilience: equities recovered from a geopolitics-driven drawdown and pushed to fresh highs, even as energy shocks and a fractured Fed kept macro uncertainty elevated. The market message looks less like “recession soon” and...

4M: Monthly Macro & Market Musings: May Flowers

April showers bring May flowers. There were not a lot of showers in April, but the flowers seemed to bloom in May anyway. May was about investing despite the noise as the S&P 500 and Nasdaq pushed to fresh record highs even as inflation ran hot, the Iran conflict flared up occasionally, and the Federal Reserve swore in a new chairman. May was first quarter earnings season and it’s those fundamentals that seemed to move the markets to new highs.

The market’s message hasn’t changed much from April: growth is intact, earnings are durable, and the energy shock is treated as a “for now” problem rather than a “forever” one. The data, however, is reminding everyone that “for now” can still sting as headline inflation hit its highest level in nearly three years. Equities are betting the war ends soon while the inflation prints show that “soon” means later, not now.

Macro: What Mattered in May

Growth: Under Pressure

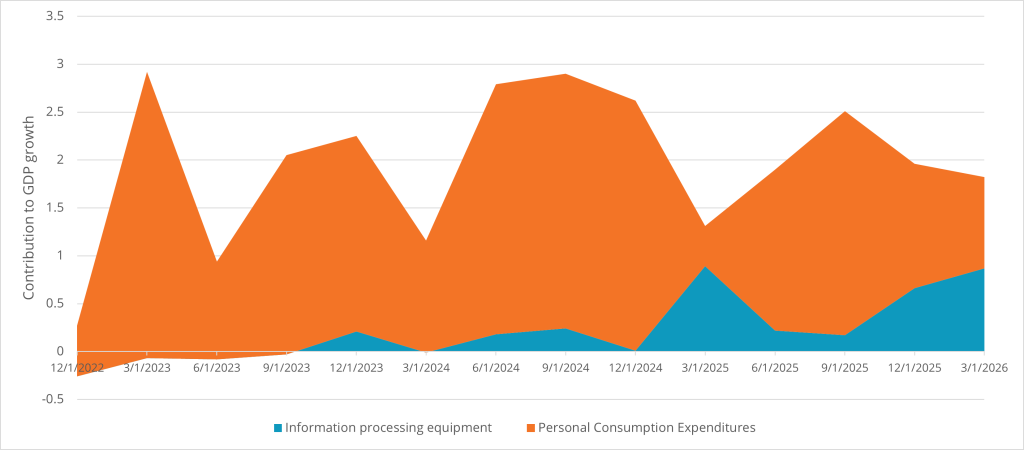

The first read on Q1 GDP landed at roughly 2% annualized, but it was just revised to 1.6%. It’s disappointing to see a downward revision, but it’s still a clear rebound from the shutdown-depressed ~0.5% pace to end 2025. The composition told the more interesting story: consumer spending cooled, government spending bounced back from the late 2025 shutdown, but business investment really surged. Equipment spending grew at its fastest clip in nearly three years, fueled by the ongoing buildout in AI and data centers.

The labor market is doing its part to keep the expansion alive. The economy added about 115,000 jobs in April and the unemployment rate held steady near 4.3%. Manufacturing even added jobs, an area seeing its first real growth since 2023. The catch is that real wages slipped as inflation ate into paychecks, which loops right back to our worry from last month: how much can an energy tax sap consumer momentum before it shows up in the spending data?

The bigger question still isn’t “is growth collapsing?” It’s how long the consumer can absorb $4.50 gas before budgets splinter? So far, the answer is “longer than the bears expected.”

What we’re watching next:

- Whether the consumer keeps fading—the Q1 slowdown in spending is the canary in the coalmine, but whether the canary dies or is just coughing depends on how long pump prices stay high.

- Whether business investment can carry the load if the consumer stumbles. The AI/capex wave and the tax incentives in the One Big Beautiful Bill Act are doing a lot of heavy lifting.

Figure 1: Q1 growth was investment-led while the consumer cooled. Business equipment spending grew at its fastest pace in nearly three years even as consumer spending slowed.

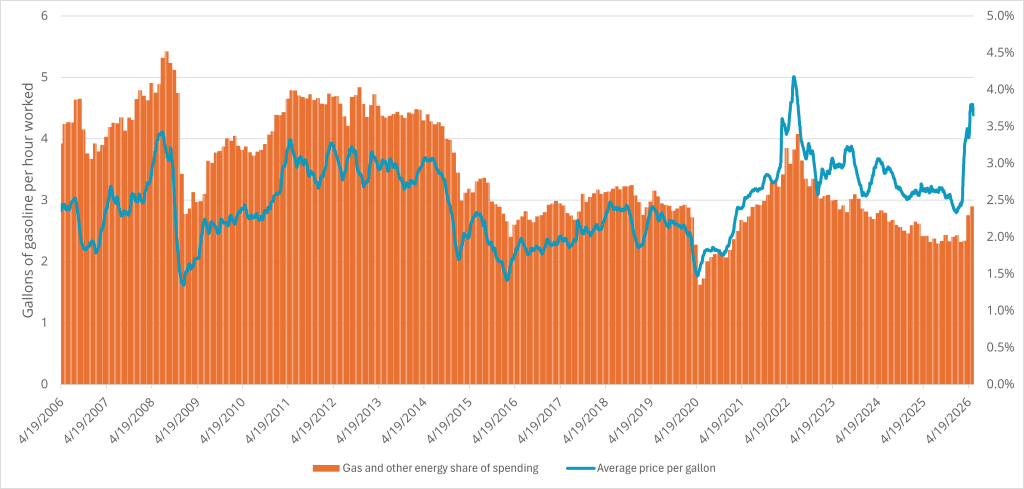

Figure 2: Gasoline crossed $4 a gallon for the first time in more than three years. The line item is small, but the squeeze on lower-income households is not.

Inflation: We Didn’t Start the Fire

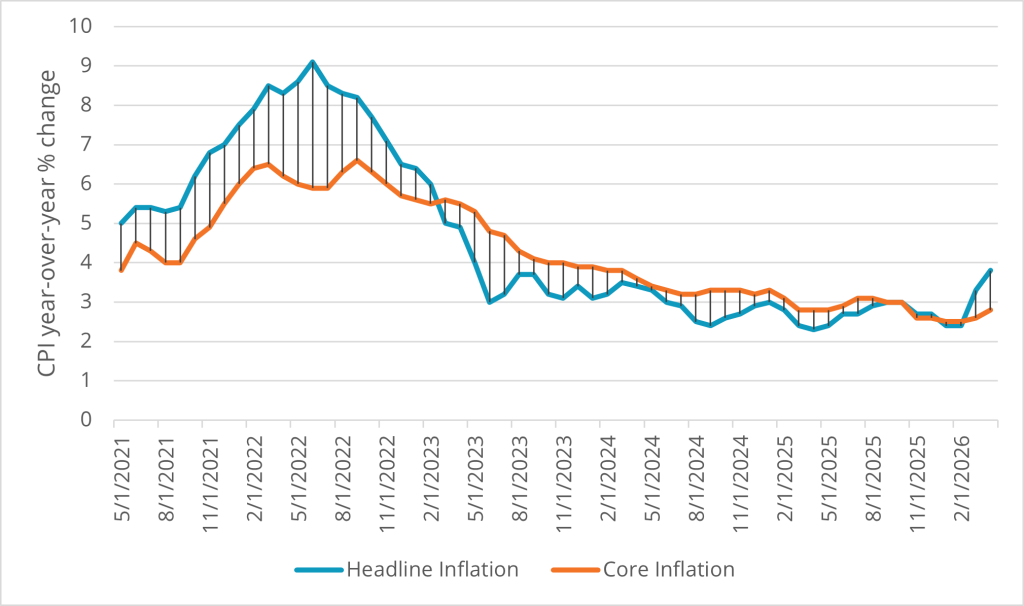

If April’s inflation print was another step backwards. The 3.8% year-over-year change in the headline consumer price index (CPI) showed that the surge in oil prices that started in late February was having a rapid response in some consumer prices—most directly, gasoline and diesel prices. Inflation hit its the hottest reading since 2023 and was the second straight month above 3%. The energy index was up nearly 18% from a year ago, with gasoline and even grocery staples (beef prices were up double digits) doing the damage.

The encouraging nuance is that core inflation (ex-food and energy) sat closer to 2.8%—elevated, but not spiraling. That gap between headline and core is the whole story: this is a supply shock, not a demand problem. The Fed didn’t start this fire; a war and a blocked shipping lane did. That distinction matters for how it eventually burns out. If oil cools from here, the headline number should drift back toward core, and core back toward 2%. The operative word remains “eventually.” Supply-driven inflation can fade fast or linger for months depending entirely on how long the disruption lasts.

Figure 3: The wedge between headline (3.8%) and core (2.8%) inflation is almost entirely energy. The fire is real, but it isn’t coming from the demand side.

Energy & Geopolitics: Stuck in the Middle

The U.S.–Iran war that has defined 2026, so far, spent May exactly where it spent April: seemingly stuck. A fragile ceasefire held in name only as Washington and Tehran traded accusations—and attacks—over the Strait of Hormuz, the chokepoint that historically carried roughly a fifth of the world’s oil and gas. Late in the month, the standoff turned hot again briefly, with reports of strikes near the strait and intercepted missiles, before diplomacy reasserted itself.

By month-end, negotiators had floated a 60-day memorandum of understanding to extend the ceasefire, begin talks on Iran’s nuclear program, and—critically for markets—restore commercial shipping through Hormuz with Iran reportedly agreeing to clear mines within 30 days. The catch: the deal still needs final sign-off, and both sides remain far apart on who actually controls the waterway.

Oil reflected the tug-of-war. West Texas Intermediate (WTI) Crude spent May swinging in the high-$80s to low-$90s, well off its panic peaks, but still dramatically higher than where 2026 began. Every headline hinting at de-escalation knocked a few dollars off; every flare-up put them right back on. The macro equation is unchanged: supply disruption plus shipping risk equals higher energy costs, which lifts inflation, saps growth, and ties the Fed’s hands. Markets can look through the fog of war so long as they believe the fog will lift. The key, as always, is recognizing that this is for now, not forever. That’s easy to say and hard to feel when you’re filling the tank.

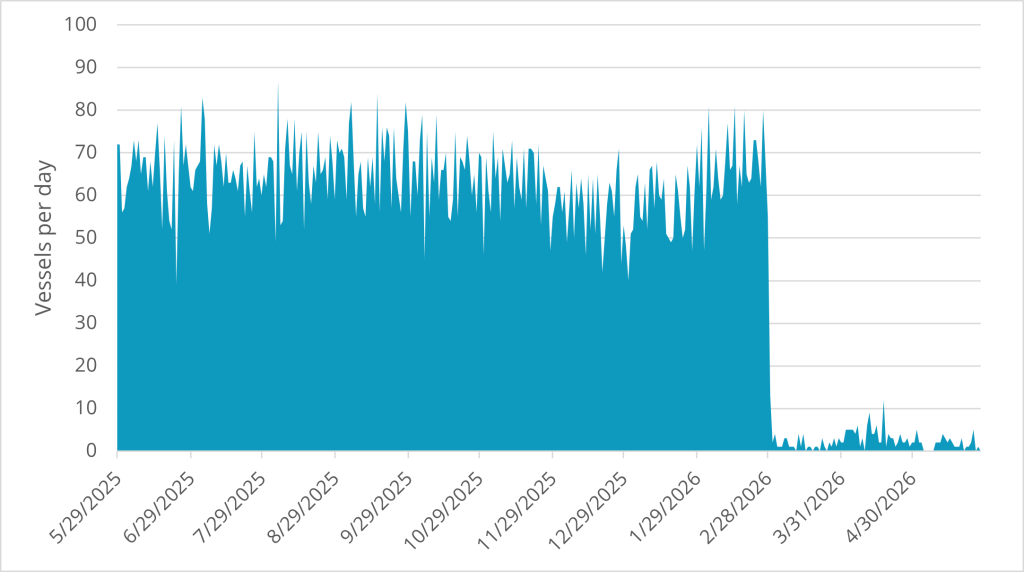

Figure 4: Tanker traffic through the Strait of Hormuz has sputtered—partial flows, then stalls—as a ceasefire is negotiated, breached, and re-negotiated. Reopening the strait is not a light switch.

The Fed: Meet the New Boss

There was no FOMC meeting in May, but the Fed still managed to make a lot of news. Kevin Warsh was sworn in as the new Fed Chair, succeeding Jerome Powell. In an unusual twist that didn’t really surprise anyone considering the circumstances around Warsh’s nomination, Powell is staying on the Board of Governors rather than leaving. As a result, ex-Chair will have a seat at the table to vote on policy.

The new boss is not the same as the old boss. For now, that probably doesn’t matter. The minutes from April’s contentious meeting (released mid-May) showed a committee that was split 8–4—the most dissents since 1992—with several members wanting to strip out any hint that the next move would be a cut, and a few openly arguing that firming could become appropriate if inflation stays above target. The new Chair has been expected to favor easier policy, but he inherits sticky, energy-driven inflation and a divided committee. When inflation is hot and the room is split, the hurdle for any major move—up or down—is high.

The result is a notable shift in market expectations. A few months ago the debate was “how many cuts?” By late May, futures markets were pricing in roughly even odds of a rate hike by year-end. That’s a remarkable turn and the equity markets didn’t seem to care. The June 17 post-meeting press conference, the first under Warsh, may make for great television.

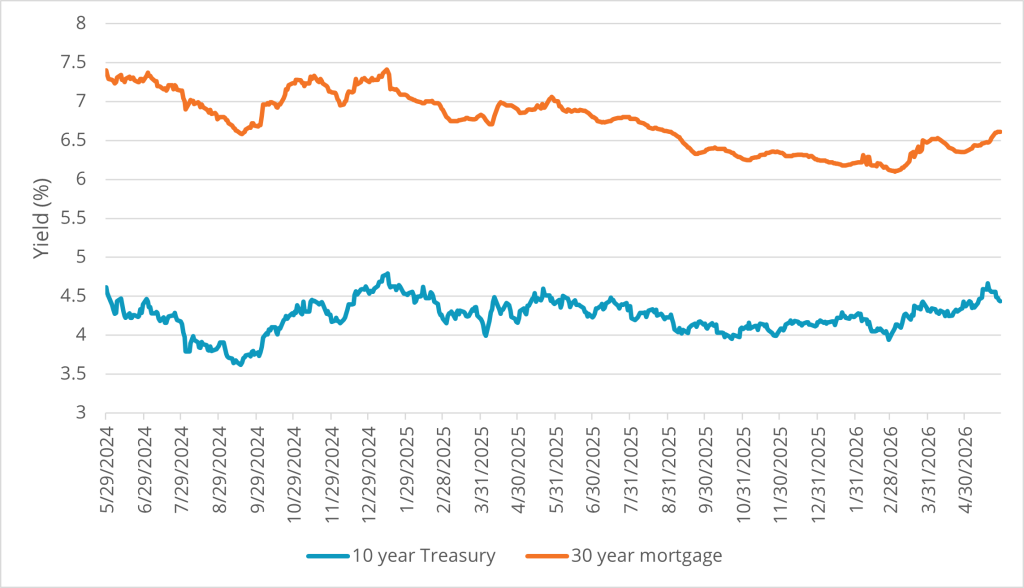

Figure 5: The 10-year yield took a round trip: a spike to a 16-month high near 4.7% on the hawkish minutes, then a retreat toward 4.5% as Iran-deal hopes pulled energy and inflation fears lower.

Markets: What the Tape Said in May

U.S. Equities: Climbing the Wall of Worry

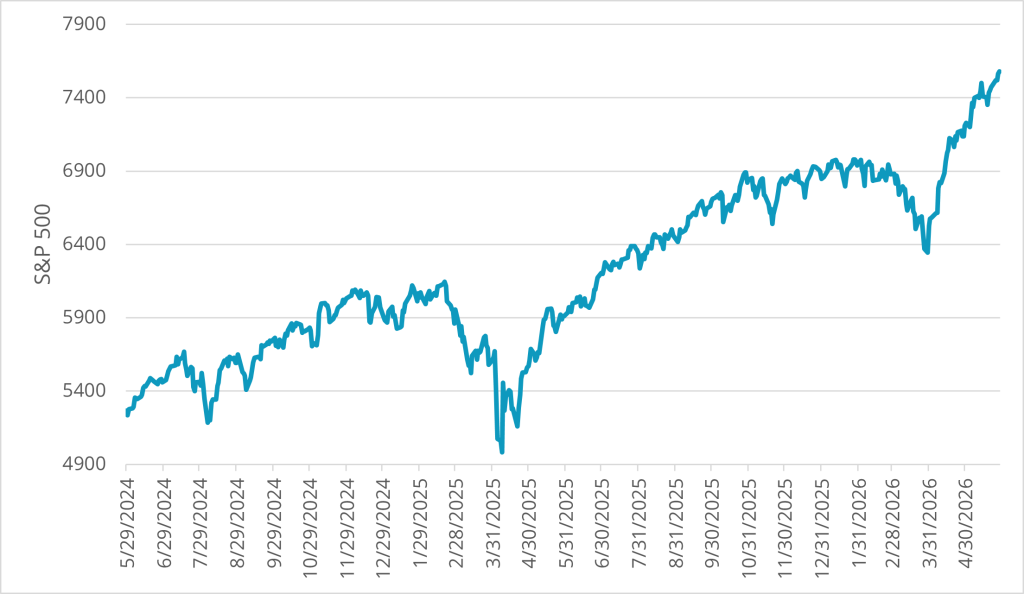

You’d be forgiven for expecting a hot inflation print, a shooting war, and a leadership change at the Fed to rattle stocks. Instead, the S&P 500 closed at a fresh record near 7,520 late in the month, with the Nasdaq notching its own all-time high. The index sits up roughly 8–9% year-to-date—a remarkable place to be given the backdrop. This is a textbook “wall of worry” the market climbs precisely because the worries are well known and loud, yet not realized. The wall of worry isn’t too steep to scale when reality defies the fears.

The fuel is earnings. First-quarter results came in strong, with profits up sharply year-over-year and the vast majority of companies beating estimates. As we noted last month, corrections (drops of 10%) are driven by fears; they typically only become bear markets (drops of 20%) when those fears become reality. Earnings resilience keeps flying in the face of the recession narrative, so the aggressive rebound shouldn’t be a shock. The risk is that the market is getting the story wrong and the trend of earnings abruptly changes. We’re not out of the woods; we’re just walking through them at a confident pace, and valuations (a forward P/E north of 21) leave little room for error.

Figure 6: The S&P 500 shrugged off the “sell in May” adage and hit new highs. The tariff shock of 2025 and the oil shock of 2026 have both, so far, rewarded holding on.

Leadership: The Trillion-Dollar Club

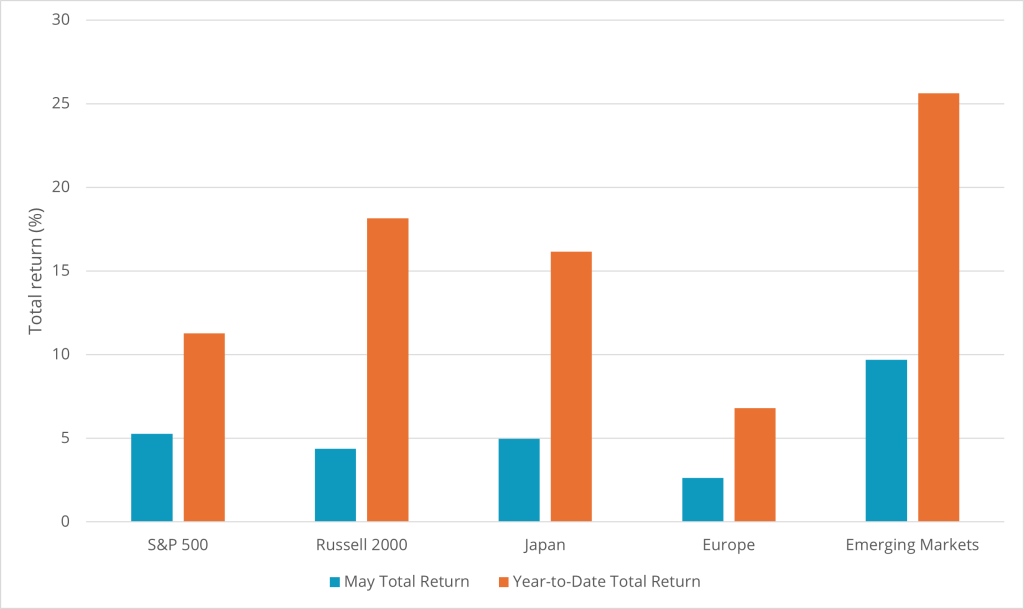

May leadership leaned right back into big tech. The AI capex story remains the market’s center of gravity—the trillion-dollar club kept growing as chipmakers and hyperscalers extended their runs, with one major memory-chip name vaulting past a $1 trillion market cap during the month. Energy, naturally, remains the year-to-date sector standout thanks to elevated oil. The encouraging, healthier theme from earlier in the year hasn’t vanished, though: small caps and non-U.S. equities have continued to participate, a reminder that leadership isn’t trapped in one narrow pocket of mega-cap tech.

Figure 7: By S&P 500 sector, Energy has led year-to-date alongside Information Technology and Communication Services. The AI trade and the oil trade have been 2026’s odd-couple leaders.

Yields: Round Trip to 4.7% and Back

If equities were calm, the bond market was anything but. The 10-year Treasury yield spiked to a 16-month high near 4.7% mid-month, pushed there by the hawkish FOMC minutes, hot inflation, and the dawning realization that the next Fed move might be a hike. But then Iran-deal optimism helped push yields lower again as lower oil prices led to cooler inflation expectations.

The takeaway from April still stands, just with a wider trading range: yields are unstable but, for now, contained. Financing conditions aren’t great, but they aren’t horrible and that matters, because the capex boom (property, plant, equipment, and an awful lot of data centers) needs to be financed. The risk is a bias higher, driven by both elevated inflation expectations and a heavy calendar of Treasury issuance. With inflation hot and the bond supply heavy, expect the whipsaw to continue, but we don’t mind having tactical positions to occasionally extend duration to take advantage of times when we’re at the upper end of the yield corridor.

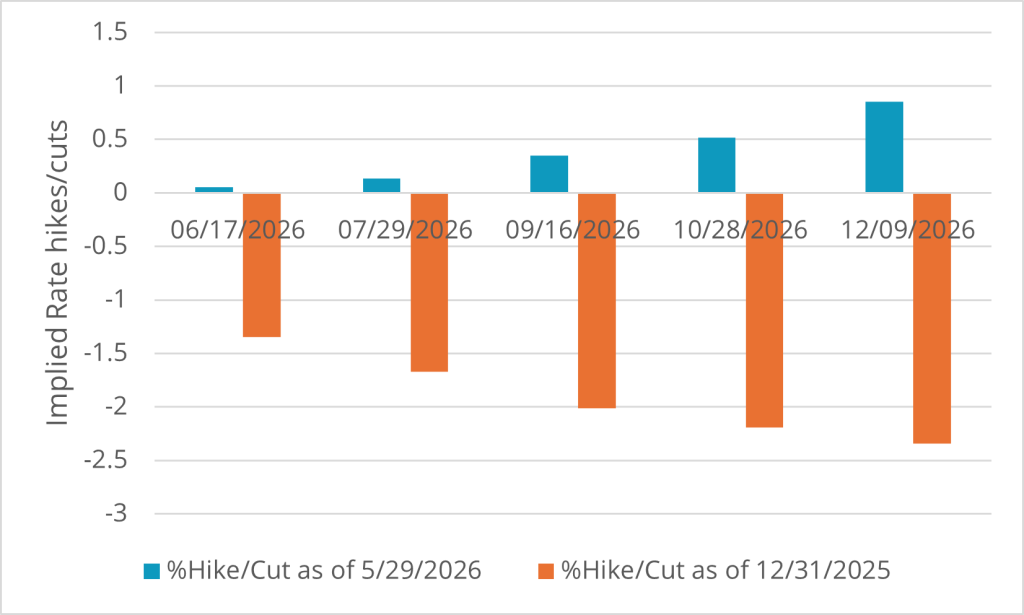

Figure 9: The market has flipped from pricing rate cuts to pricing a meaningful chance of a hike by year-end. The implied path for the funds rate has tilted up, not down.

What This Means for Positioning: Main Takeaways

- Energy is still the swing factor. A genuine, durable Hormuz reopening would be disinflationary and supportive for both stocks and bonds. A breakdown in the deal is the clearest path to the next drawdown.

- The Fed has a new chair but the same dilemma. Meet the new boss, who still has to wrestle hot, energy-driven inflation and a split committee. Don’t assume the leadership change means imminent cuts; the market is now flirting with the opposite. June’s meeting is the one to watch.

- Watch the consumer, not just the headline. Q1’s spending slowdown and shrinking real wages are the soft underbelly of an otherwise solid economy. Strong earnings can’t fully offset a tired consumer forever.

- Breadth is still a feature, not a bug. Small caps and international names continue to pull their weight. Diversification keeps earning its keep, even in a market led by the trillion-dollar club.

- Yields are attractive, but they could get more so. The round trip to 4.7% was a reminder that the locked-in-yield opportunity hasn’t closed. For those who feel they missed it, the issuance-and-inflation backdrop may hand out more chances.